Behavior and Factors Influencing Debt Accumulation through SPayLater Service among Undergraduate Students in Bangkok and Metropolitan Areas

Keywords:

SPayLater, Debt Accumulation Behavior, Debt Repayment AbilityAbstract

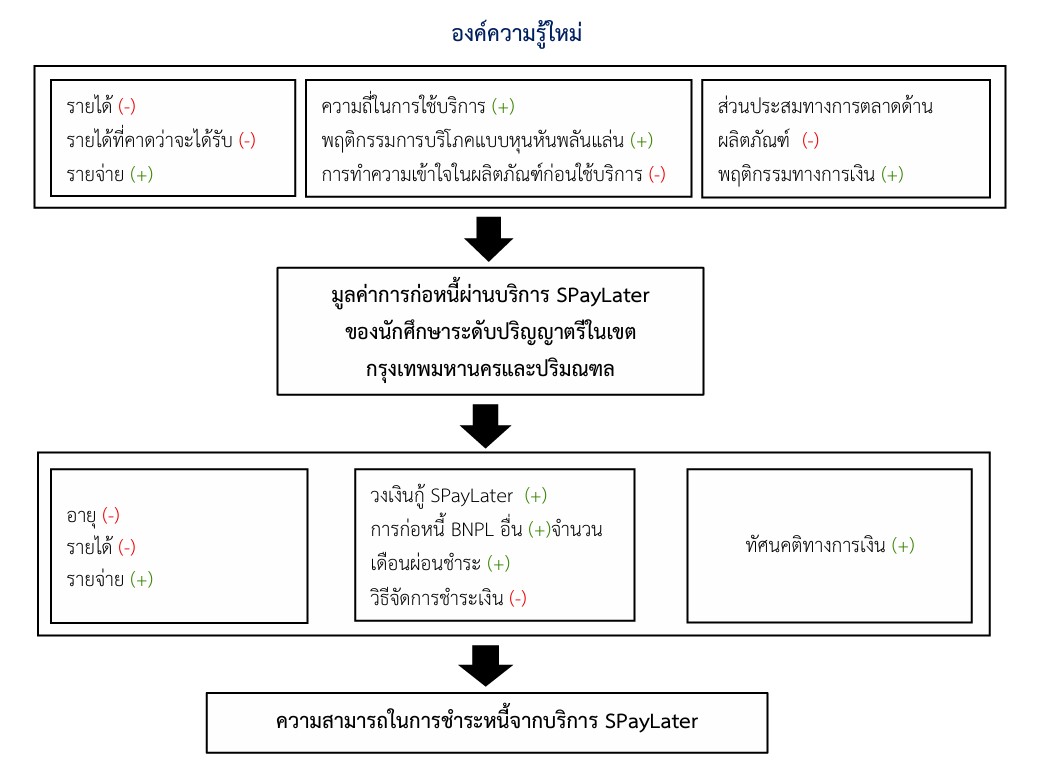

This research aimed to (1) study the behaviors and factors influencing debt accumulation through the SPayLater service among undergraduate students in Bangkok and its metropolitan area, and (2) analyze the factors affecting the ability to repay debts through this service. This quantitative study sampled 400 participants using stratified sampling based on the type of educational institution, including (1) open-admission public universities, (2) Rajabhat universities and Rajamangala University of Technology, (3) autonomous and limited-admission public universities, and (4) private universities. Quota sampling was then applied to select 100 participants from each category, and data were collected via convenience sampling. The instrument used was a questionnaire. Data analysis involved descriptive and inferential statistics, including mean, percentage, maximum-minimum values, standard deviation, multiple regression analysis, and logistic regression analysis. The results revealed that (1) factors significantly associated with debt accumulation through SPayLater include income level, expenditure level, expected income, frequency of service usage, impulsive spending behavior, product literacy, product factors, and financial behaviors; (2) factors significantly influencing debt default through SPayLater include age, income level, expenditure level, debt behavior via buy-now-pay-later service, approved credit limit, chosen installment period, payment management methods, and financial attitudes. Based on these findings, policy recommendations suggest that the private sector should develop automated payment and notification systems; the public should be promoted to enhance financial skills to avoid unplanned debt behavior; and the government should integrate financial knowledge into the education system and appropriately regulate digital credit for groups with unstable incomes.

References

กลุ่มธุรกิจการเงินธนาคารเกียรตินาคินภัทร. (2564). แผ่สมรภูมิ E-commerce ไทย ตรงไหนคือโอกาส. สืบค้นจาก https://advicecenter.kkpfg.com/th/kkp-research/e-commerce-situation-in-thailand.

กัลยา วาณิชย์บัญชา และ ฐิตา วานิชย์บัญชา. (2564). การใช้ SPSS ในการวิเคราะห์ข้อมูล. กรุงเทพฯ: สามลดา.

ณิชาภา สุตพล. (2562). ปัจจัยที่มีอิทธิพลต่อพฤติกรรมการชำระหนี้บัตรเครดิตในช่วงสถานการณ์ COVID-19 ของประชากรในเขตกรงเทพมหานคร. (บริหารธุรกิจมหาบัณฑิต, มหาวิทยาลัยรามคำแหง).

ธนัชชา แก้วสลับศรี, ชิดตะวัน ชนะกุล และ มานะ ลักษมีอรุโณทัย. (2566). ปัจจัยที่ส่งผลต่อระยะเวลาการผิดนัดชำระหนี้ของผู้กู้ยืมเงินกองทุนเงินให้กู้ยืมเพื่อการศึกษา. วารสารสังคมศาสตร์ปัญญาพัฒน์, 5(4), 1–12.

ธนาคารแห่งประเทศไทย. (2565). รายงานสำรวจทักษะทางการเงินของไทย ปี 2565. สืบค้นจาก https://www.bot.or.th/th/research-and-publications/articles-and-publications/bot-magazine/Phrasiam-67-2/2567-info-financial-skill.html.

ธนาคารแห่งประเทศไทย. (2565ข). หนี้ครัวเรือนไทย วิกฤตแค่ไหน ทำไมถึงไม่ควรมองข้าม. สืบค้นจาก https://projects.pier.or.th/household-debt/.

พรภัทร อินทรวรพัฒน์, สิรีรัตน์เชษฐสุมน และ ผ่องพรรณ ตรัยมงคลกูล. (2557). ปัจจัยเชิงสาเหตุที่มีอิทธิพลต่อการก่อหนี้ของนักศึกษาระดับปริญญาตรีในเขตกรุงเทพมหานคร. วารสารเกษตรศาสตร์ (สังคม), 35(1), 1-15.

เพ็ญพิชชา สกลวิทยานนท์. (2565). ปัจจัยที่มีอิทธิพลต่อการตัดสินใจใช้รูปแบบการชำระเงินซื้อก่อนจ่ายทีหลัง (BNPL) กรณีศึกษา Shopee SPayLater. (เศรษฐศาสตรมหาบัณฑิต, มหาวิทยาลัยธรรมศาสตร์).

แพรวไพลิน จันทรโพธิ์ศรี, วิชนี เอี่ยมชุ่ม และ เบญจมาภรณ์ สมบัติธีระ. (2566). ปัจจัยที่มีอิทธิพลต่อการเป็นหนี้ของครัวเรือนเกษตรกร กรณีศึกษา อำเภอบรบือ จังหวัดมหาสารคาม. วารสารการจัดการและพัฒนา มหาวิทยาลัยราชภัฏอุบลราชธานี, 11(1), 227–240.

วรณัฏฐกานต์ นุชพุ่ม. (2567). ปัจจัยที่มีอิทธิพลต่อพฤติกรรมการชำระหนี้บัตรเครดิต ธนาคารไทยพาณิชย์ในเขตกรุงเทพมหานคร. (เศรษฐศาสตรมหาบัณฑิต, มหาวิทยาลัยธุรกิจบัณฑิตย์).

อักขราวรรณ อักขระชาตะ. (2565). ปัจจัยที่ส่งผลต่อพฤติกรรมการใช้ SPayLater ของแอปพลิเคชัน Shopee ของประชาชนช่วงอายุ 18-25 ปี ในเขตกรุงเทพมหานคร. (บริหารธุรกิจมหาบัณฑิต, มหาวิทยาลัยรามคำแหง).

Bank for International Settlements. (2016). The real effects of household debt in the short and long run. Retrieved from https://www.bis.org/publ/work607.html.

Cochran, W. G. (1953). Sampling techniques. (2nd ed.). New York: John Wiley & Sons.

Fauza, H. (2023). Get it fast, pay it later: Analysis of paylater features as a support of the Generation Z lifestyle. Jurnal Pendidikan Sosial dan Ekonomi, 12(1), 71–83.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Journal of Social Science Panyapat

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.