The Influence of Internal Control and Internal Audit on Financial Report Quality of Local Administrative Organizations in The Northeastern Region

Keywords:

Internal Control, Internal Audit, Financial Report QualityAbstract

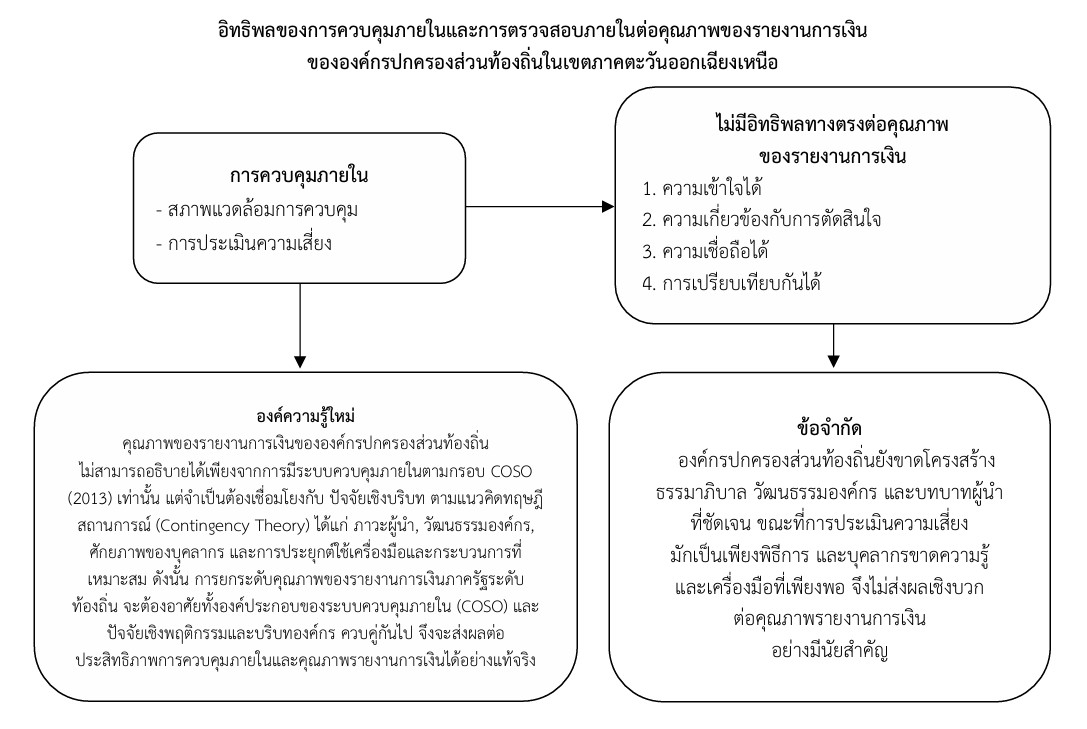

This research article aims to examine (1) the influence of internal control on financial reporting quality and (2) the influence of internal audit on the financial reporting quality of local administrative organizations in the Northeastern region of Thailand. A quantitative research method was employed, and data were collected from 268 local government officials serving as Senior Professional Internal Auditors or Professional Internal Auditors within these organizations. A structured questionnaire was used as the data collection tool. The data were analyzed using descriptive statistics, including percentages, means, frequencies, and standard deviations, as well as multiple regression analysis to test the research hypotheses. The findings revealed that internal control, particularly in the areas of control activities, information and communication, and monitoring and evaluation, had a statistically significant positive direct influence on financial reporting quality. However, the components of the control environment and risk assessment did not demonstrate a statistically significant influence. Additionally, internal audit, which includes audit planning, audit execution, and reporting and follow-up, also had a statistically significant positive direct influence on the financial reporting quality of local administrative organizations in the region.

References

กระทรวงการคลัง. (2561). มาตรฐานการบัญชีภาครัฐและนโยบายการบัญชีภาครัฐ พ.ศ. 2561. สืบค้นจาก https://url.in.th/IrlZG.

จิตรลดา สีหามาตย์. (2561). ความสัมพันธ์ของประสิทธิภาพการควบคุมภายในที่มีต่อคุณภาพรายงานทางการเงินของหน่วยงานภาครัฐในมุมมองของเจ้าหน้าที่ตรวจสอบของสำนักงานการตรวจเงินแผ่นดิน. (บัญชีมหาบัณฑิต, มหาวิทยาลัยศรีปทุม).

ธนพล อินต๊ะขัน และ กรวีร์ ชัยอมรไพศาล. (2565). ผลกระทบของการควบคุมภายในตามกรอบมาตรฐานสากลต่อผลการดำเนินงาน ขององค์กรปกครองส่วนท้องถิ่นในจังหวัดเชียงใหม่. วารสารบริหารธุรกิจและศิลปศาสตร์ ราชมงคลล้านนา, 10(2), 19–36.

น้ำผึ้ง เรืองสุวรรณ. (2562). ผลของการควบคุมภายในที่มีต่อประสิทธิภาพการใช้งานด้านระบบสารสนเทศทางการบัญชีของมหาวิทยาลัยในกำกับของรัฐ. (บัญชีมหาบัณฑิต, มหาวิทยาลัยศรีปทุม).

เนาวรัตน์ เทพรักษ์. (2565). การควบคุมภายในและการตรวจสอบทางการเงินส่งผลต่อประสิทธิภาพการปฏิบัติงานของสำนักงานอัยการสูงสุด. (บัญชีมหาบัณฑิต, มหาวิทยาลัยศรีปทุม).

บุญชม ศรีสะอาด. (2560). การวิจัยเบื้องต้น. (พิมพ์ครั้งที่ 10). กรุงเทพฯ: สุวีริยาสาสน์.

เบญญาภา วงศ์กองแก้ว. (2563). การควบคุมภายในตามกรอบแนวคิดของโคโซ่ (Committee of Sponsoring Organizations of The Treadway Commission) และการจัดการความเสี่ยงที่ส่งผลต่อประสิทธิภาพการปฏิบัติงานของบุคลากรหน่วยงานของรัฐในภาคเหนือตอนล่าง. (บัญชีมหาบัณฑิต, มหาวิทยาลัยศรีปทุม).

ปรียานุช สอนซ้าย และ สายทิพย์ จะโนภาษ. (2564). ผลกระทบของการควบคุมภายในการจัดซื้อจัดจ้างที่มีต่อประสิทธิผล การบริหารงบประมาณขององค์กรปกครองส่วนท้องถิ่นในภาคตะวันออกเฉียงเหนือตอนบน 2. วารสารการบัญชีและการจัดการ, 13(4), 24–37.

ปิ่นฤทัย เจียมทอง, ประนอม คำผา และ อโณทัย หาระสาร. (2566). ปัจจัยที่ส่งผลต่อคุณภาพรายงานการเงินขององค์กรปกครองส่วนท้องถิ่นในมุมมอง ของผู้ตรวจสอบสำนักงานการตรวจเงินแผ่นดิน ในภาคตะวันออกเฉียงเหนือ. วารสารการจัดการและพัฒนา มหาวิทยาลัยราชภัฏอุบลราชธานี, 10(1), 149–165.

สำนักงานการตรวจเงินแผ่นดิน. (2566). รายงานผลการปฏิบัติงาน ประจำปีงบประมาณ พ.ศ. 2566. สืบค้นจาก https://shorturl.asia/bFths.

สิริพรรณ์ โกมลรัตน์มงคล. (2563). ปัจจัยที่ส่งผลต่อคุณภาพรายงานทางการเงินของรัฐวิสาหกิจในประเทศไทย. (บัญชีมหาบัณฑิต, มหาวิทยาลัยศรีปทุม).

Agbenyo, W., Jiang, Y., & Cobblah, P. K. (2018). Assessment of government internal control systems on financial reporting quality in Ghana: A case study of Ghana revenue authority. International Journal of Economics and Finance, 10(11), 40-50.

Beest, F. V., Braam, G., & Boelens, S. (2009). Quality of financial reporting: Measuring qualitative characteristics. Retrieved from https://repository.ubn.ru.nl/bitstream/handle/2066/74896/74896.pdf.

Committee of Sponsoring Organizations of The Treadway Commission. (2013). Internal control—Integrated framework. Englewood Cliffs, New Jersey: Committee of Sponsoring Organizations of The Treadway Commission.

Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting earnings management. Accounting review, 70(2), 193–225.

Dechow, P., Ge, W., & Schrand, C. (2010). Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of accounting and economics, 50(2-3), 344-401.

Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics. (5th ed.). New York: McGraw-Hill Irwin.

Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2019). Multivariate data analysis. (8th ed.). Boston, Massachusetts: Cengage Learning.

Kewo, C. L. (2017). The influence of internal control implementation and managerial performance on financial accountability local government in Indonesia. International Journal of Economics and Financial Issues, 7(1), 293-297.

Kewo, C. L., & Afiah, N. N. (2017). Does quality of financial statement affected by internal control system and internal audit?. International Journal of Economics and Financial Issues, 7(2), 568-573.

Rovinelli, R. J., & Hambleton, R. K. (1977). On the use of content specialists in the assessment of criterion-referenced test item validity. Retrieved from https://eric.ed.gov/?id=ED121845.

Tambingon, H. N., Yadiati, W., & Kewo, C. L. (2018). Determinant factors influencing the quality of financial reporting local government in Indonesia. International Journal of Economics and Financial Issues, 8(2), 262-268.

Yamane, T. (1973). Statistics: An Introductory Analysis. (3rd ed.). New York: Harper & Row.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Journal of Social Science Panyapat

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.