The Working Environment and Auditors’ Competency Affecting The Performance Efficiency of Tax Audit Officers in Bangkok Area

Keywords:

Working Environment, Auditor’s Competency, EfficiencyAbstract

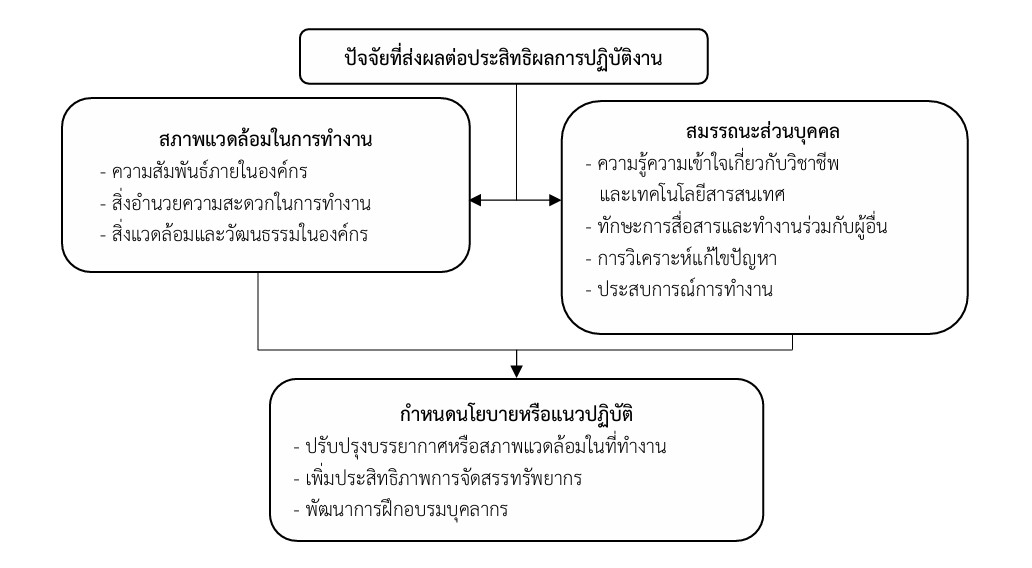

This research article aims to investigate: (1) the working environment affecting the performance efficiency of tax auditors, and (2) the competence of auditors impacting the performance efficiency of tax auditors in the Bangkok area. This study employed a quantitative research design. The sample consisted of 330 tax auditors in the Bangkok area. Data were collected using questionnaires. The statistical analyses used included frequency, percentage, standard deviation, and Pearson correlation analysis. Subsequently, the collected data were analyzed using multiple regression analysis. The study findings revealed that: (1) the working environment had a positive influence on the performance efficiency of tax auditors in the Bangkok area across all aspects. The working environment significantly promoted the quality and quantity of completed work, time spent on tasks, and the amount of tax collected, with a statistical significance of 0.05. (2) The competence of auditors also had a positive influence on the performance efficiency of tax auditors in the Bangkok area in all aspects, including work quality, quantity of completed work, time spent on tasks, and the amount of tax collected, with a statistical significance of 0.05.

References

กรมสรรพากร. (2567). เกี่ยวกับกรมสรรพากร. สืบค้นจาก https://www.rd.go.th/327.html.

จิรภรณ์ รังคสิริ และ สวัสดิ์ วรรณรัตน์. (2562). องค์ประกอบหลักการจัดเก็บภาษีที่ดีของสำนักงานสรรพากรพื้นที่กรุงเทพมหานคร. วารสารวิชาการมหาวิทยาลัยการจัดการและเทคโนโลยีอีสเทิร์น, 16(1), 265-273.

ชาคริต ศรีขาว. (2551). ความคิดเห็นต่อประสิทธิภาพในการปฏิบัติงานของพนักงาน บริษัท มิสกัน (ไทยแลนด์) จํากัด. (บริหารธุรกิจมหาบัณฑิต, มหาวิทยาลัยราชภัฏพระนครศรีอยุธยา).

นุชจรี นักไร่. (2564). ความสัมพันธ์ระหว่างความเกี่ยวข้องของงานในสภาพแวดล้อมที่สามารถตรวจสอบกับคุณภาพการดูแลของพยาบาลโรงพยาบาลมหาวิทยาลัย. (พยาบาลศาสตรมหาบัณฑิต, จุฬาลงกรณ์มหาวิทยาลัย).

พรปวีณ์ ภูมิวงค์, ประเวศ เพ็ญวุฒิกุล และ ถิรวุฒิ ยังสุข. (2567). สมรรถนะของนักตรวจสอบภาษีและแรงจูงใจที่ส่งผลต่อความสำเร็จ ในการปฏิบัติงานของนักตรวจสอบภาษีในสำนักงานสรรพากร ภาค 3. วารสารวิชาการสังคมศาสตร์เครือข่ายวิจัยประชาชื่น, 6(2), 20–37.

พัชรนันท์ จิระวัฒนภิญโญ. (2562). ปัจจัยที่มีอิทธิพลต่อการปฏิบัติงานตามหลักธรรมาภิบาลของ บุคลากร กรมปศุสัตว์สังกัดส่วนภูมิภาคในพื้นที่เขต 4. ขอนแก่น: สำนักงานปศุสัตว์เขต 4.

รัตติยา เปรื่องประยูร. (2565). ทักษะการตรวจสอบภาษีและสภาพแวดล้อมในการทำงานที่ส่งผลต่อประสิทธิภาพการปฏิบัติงานของนักตรวจสอบภาษีสรรพากรภาค 1. (บัญชีมหาบัณฑิต, มหาวิทยาลัยศรีปทุม).

สำนักงานสถิติแห่งชาติ. (2566). ข้อมูลสถิติกรุงเทพ ด้านเศรษฐกิจ, ข้อมูลสถิติกรุงเทพมหานคร พ.ศ.2566. สืบค้นจาก https://www.nso.go.th/public/e-book/Other-Publications/Bangkok_Statistical_Data_2566/58/.

สุรพงษ์ คงสัตย์ และ ธีรชาติ ธรรมวงค์. (2551). การหาค่าความเที่ยงตรงของแบบสอบถาม (IOC). สืบค้นจาก https://www.mcu.ac.th/article/detail/14329.

อิศราภรณ์ ตุงใย. (2567). ปัจจัยการปฏิบัติงานและสภาพแวดล้อมที่ส่งผลต่อประสิทธิภาพการจัดเก็บภาษี ของสำนักงานสรรพากร ภาค 4. วารสารรัฐศาสตร์ มหาวิทยาลัยราชภัฏสวนสุนันทา, 7(2), 106–122.

Diamantidis, A. D., & Chatzoglou, P. (2019). Factors affecting employee performance: an empirical approach. International journal of productivity and performance management, 68(1), 171-193.

Han, Z. (2024). Research on the relationship between intellectual capital, supply chain knowledge sharing and enterprise innovation ability. Trends in Social Sciences and Humanities Research, 2(8), 17-26.

McClelland, D. C. (1973). Testing for competence rather than for “intelligence”. American psychologist, 28(1), 1–14.

Yamane, T. (1973). Statistics: An Introductory Analysis. (3rd ed.). New York: Harper & Row.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Journal of Social Science Panyapat

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.