The Impact of Leverage on Magnitude of Earnings Management of Listed Companies on The Stock Exchange of Thailand, SET100

Keywords:

Leverage, Earnings Management, SET100 Index GroupAbstract

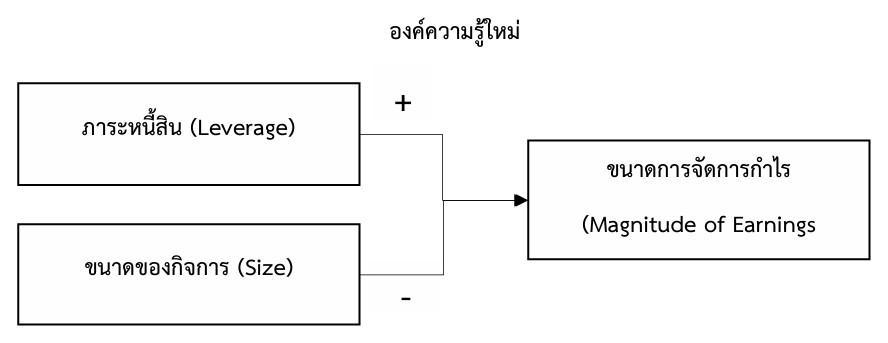

This study aims to examine the impact of leverage (LEV) on the magnitude of earnings management (MEM) of companies listed on the Stock Exchange of Thailand (SET) within the SET100 index during the years 2020 to 2023. Secondary data were collected from annual reports, financial statements, and the SET SMART database. The sample consisted of panel data comprising 340 firm-year observations. The data analysis involved descriptive statistics and multiple regression analysis. The results revealed that leverage has a positive and statistically significant effect on earnings management, indicating that companies with higher leverage tend to engage in earnings management to enhance their financial image. This finding is consistent with agency theory and contracting theory, which suggest that pressure from leverage influences earnings management behavior. The results of this study can be used as information for investors, creditors, and regulators to assess risks and promote transparency in financial reporting.

References

กัลยา วานิชย์บัญชา. (2559). การวิเคราะห์สถิติ: สถิติสำหรับบริหารและวิจัย. (พิมพ์ครั้งที่ 16). กรุงเทพฯ: จุฬาลงกรณ์มหาวิทยาลัย.

ปฐมพงค์ กุกแก้ว และ พิธาน แสนภักดี. (2565). ปัจจัยที่มีอิทธิพลต่อการจัดการกำไรของธุรกิจบริการที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารวิทยาการจัดการ มหาวิทยาลัยราชภัฏอุดรธานี, 4(3), 29–41.

ปิยะรัตน์ โพธิ์ย้อย, พัทธนันท์ เพชรเชิดชู และ ศิริเดช คำสุพรหม. (2563). ปัจจัยที่มีอิทธิพลต่อโครงสร้างเงินทุนของบริษัทจดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย กลุ่ม SET100. วารสารสุทธิปริทัศน์, 34(112), 140–161.

ปิยาภิศักดิ์ เจียรสุคนธ์. (2565). การเปรียบเทียบลักษณะพฤติกรรมของผู้บริหารในการบิดเบือนข้อมูลทางบัญชีของกลุ่มบริษัทจดทะเบียนที่ถูกและไม่ถูกสำนักงาน ก.ล.ต. สั่งให้แก้ไขงบการเงินและตรวจสอบเป็นกรณีพิเศษ. วารสารศิลปศาสตร์และวิทยาการจัดการ มหาวิทยาลัยเกษตรศาสตร์, 9(2), 81–97.

เปรมารัช วิลาลัย, พัทธนันท์ เพชรเชิดชู และ ศิริเดช คำสุพรหม. (2563). การจัดการกำไรผ่านการใช้ดุลยพินิจในการสร้างรายการทางธุรกิจ และการจัดการกำไรผ่านรายการคงค้าง กับความสามารถในการทำกำไรในอนาคต. วารสารการบัญชีและการจัดการ, 12(3), 83–96.

สุทิน ชนะบุญ. (2560). สถิติและการวิเคราะห์ข้อมูลในงานวิจัยเบื้องต้น. สืบค้นจาก http://kkpho.go.th/km/index.php/2017-08-10-06-37-01/category/2-r2r-5.

Dechow, P. M., Sloan, R. G., & Sweeney, A. P. (1995). Detecting earnings management. Accounting review, 70(2), 193-225.

Hoang, K. M. T., & Phung, T. A. (2019). The effect of financial leverage on real and accrual-based earnings management in Vietnamese firms. Economics & Sociology, 12(4), 299-333.

Jelinek, K. (2007). The effect of leverage increases on earnings management. The Journal of Business and Economic Studies, 13(2), 24.

Jensen, M. C., & Meckling, W. H. (2019). Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. In Corporate Governance (pp. 77-132). Hampshire: Gower.

Ujah, N. U., & Brusa, J. (2014). Earnings management, financial leverage, and cash flow volatility: An analysis by Industry. Journal of Business and Economics, 5(3), 338-348.

Watts, R. L., & Zimmerman, J. L. (1986). Positive accounting theory. Englewood Cliffs, NJ: Prentice Hall.

Zagers-Mamedova, I. (2009). The effect of leverage increases on real earnings management. Retrieved from http://hdl.handle.net/1765/15572.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Journal of Social Science Panyapat

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.