The Relationship between Board Structure, Sustainability Disclosure, and Financial Performance of Thai Commercial Banks Listed on the Stock Exchange of Thailand (2014–2023)

Keywords:

Board Structure, Sustainability Disclosure, Financial Performance, Thai Commercial BanksAbstract

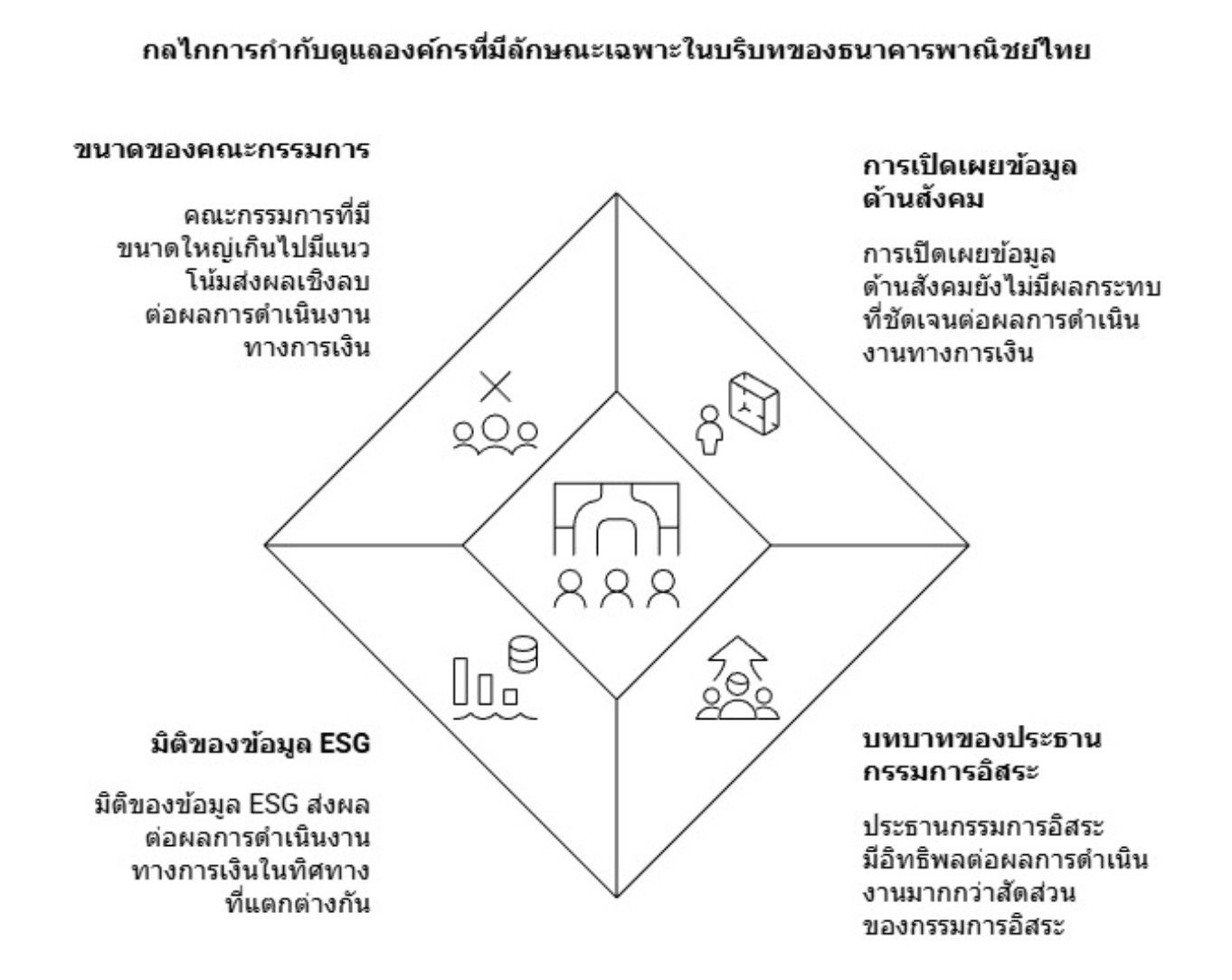

This study examines the relationship between board structure, sustainability disclosure, and the financial performance of Thai commercial banks listed on the Stock Exchange of Thailand. Given the growing importance of corporate governance and sustainability in the banking sector, this research employs panel data covering the period from 2014 to 2023. The key independent variables include board size, board independence, independent chairmanship, and sustainability disclosure across economic, environmental, and social dimensions. Panel data regression techniques were applied, with fixed-effects or random-effects models selected according to appropriate statistical tests. The results indicate that board structure is associated with financial performance only in certain dimensions, with board size and independent chairmanship exhibiting differential effects across financial performance indicators. In addition, sustainability disclosure is found to be related to financial performance in a non-uniform manner. Economic, environmental, and social disclosure dimensions show significant associations with specific financial performance measures, while no consistent relationship is observed across all indicators. Overall, the findings suggest that both board structure and sustainability disclosure are linked to the financial performance of Thai commercial banks in a selective and dimension-specific manner. The results provide empirical support for the proposed research framework and indicate that the effects of corporate governance and sustainability disclosure on financial performance depend on the specific dimensions and performance measures considered.

References

Baltagi, B. H. (2008). Econometric analysis of panel data. (4th ed.). New Jersey: John Wiley & Sons.

Bryman, A. (2016). Social research methods. (5th ed.). Oxford: Oxford University Press.

Freeman, R. E. (1984). Strategic management: A stakeholder approach. New Jersey: Pitman.

Freeman, R. E., Harrison, J. S., Wicks, A. C., Parmar, B. L., & De Colle, S. (2010). Stakeholder theory: The state of the art. Cambridge: Cambridge University Press.

Frias‐Aceituno, J. V., Rodriguez‐Ariza, L., & Garcia‐Sanchez, I. M. (2013). The role of the board in the dissemination of integrated corporate social reporting. Corporate social responsibility and environmental management, 20(4), 219-233.

Global Reporting Initiative. (2021). GRI Universal Standards 2021. Retrieved from https://www.globalreporting.org/standards.

Gujarati, D. N., & Porter, D. C. (2009). Basic econometrics. (5th ed.). New York: McGraw-Hill.

Hair, J. F., Black, W. C., Babin, B. J., & Anderson, R. E. (2019). Multivariate data analysis. (8th ed.). Upper Saddle River: Cengage Learning.

Haniffa, R. M., & Cooke, T. E. (2002). Culture, corporate governance and disclosure in Malaysian corporations. Abacus, 38(3), 317-349.

Jensen, M. C., & Meckling, W. H. (2019). Theory of the firm: Managerial behavior, agency costs and ownership structure. In Tricker, R.I. (Ed.), Corporate governance (pp. 77-132). Surrey: Gower.

KPMG. (2022). The time has come: The KPMG survey of sustainability reporting 2022. KPMG International. Retrieved from https://home.kpmg/xx/en/home/insights/2022/09/the-time-has-come-survey-of-sustainability-reporting.html.

Lipton, M., & Lorsch, J. W. (1992). A modest proposal for improved corporate governance. Business Lawyer, 48(1), 59–77.

Mallin, C. A. (2019). Corporate governance. (6th ed.). Oxford: Oxford University Press.

Securities and Exchange Commission, Thailand. (2020a). Form 56-1 One Report: Annual registration statement. Bangkok: SEC.

Securities and Exchange Commission, Thailand. (2020b). Guidelines for sustainability disclosure. Bangkok: SEC.

Sekaran, U., & Bougie, R. (2016). Research methods for business: A skill-building approach. (7th ed.). New Jersey: Wiley.

The Stock Exchange of Thailand. (2014–2023). Annual financial statements of listed Thai commercial banks. Bangkok: SET.

The Stock Exchange of Thailand. (2023). SET Sustainability reporting guidelines. Bangkok: SET.

Velte, P. (2017). Does ESG performance have an impact on financial performance? Evidence from Germany. Journal of Global Responsibility, 8(2), 169–178.

Wooldridge, J. M. (2010). Econometric analysis of cross section and panel data. (2nd ed.). Massachusetts: MIT Press.

World Bank. (2024). Sustainability and climate disclosures in financial institutions: Global practices andlessons for Asia. Washington, D.C.: World Bank Group.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Journal of Social Science Panyapat

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.