Determinants of Liquid Assets in Large Savings Cooperatives from 2019-2023

Keywords:

Saving Cooperatives, Liquidity, Financial FactorsAbstract

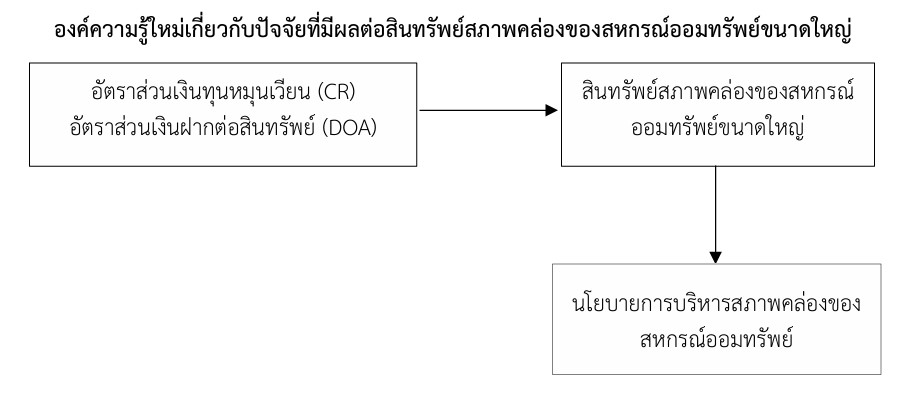

This article aimed to study the factors affecting the liquidity of assets in large savings cooperatives. The study employs multiple regression analysis using the stepwise method. The data were obtained from the financial statements of large savings cooperatives as presented in their annual reports. The cooperatives included in the study are those that operated during the fiscal years 2019–2023, totaling 141 cooperatives. Total assets (TA) are included as a control variable in the analysis. The study found that the factors influencing the level of liquidity assets in large savings cooperatives include The Current Ratio (CR) shows a statistically significant positive effect, with a coefficient of 1.305, indicating a positive impact on maintaining liquidity assets in large savings cooperatives. This reflects their ability to meet short-term debts promptly. Furthermore, the Deposit to Assets Ratio (DOA) also positively affects the level of liquidity assets, with a coefficient of 1.929 and statistical significance. This indicates that cooperatives with higher member deposits naturally maintain greater liquidity assets for effective management. This indicates that when cooperatives have a strong ability to meet short-term obligations or receive a large amount of deposits from members, they tend to possess higher liquidity assets for management and operations. This study reflects a management structure that prioritizes stability over profit maximization in cooperatives.

References

กรมส่งเสริมสหกรณ์. (2550). นโยบายส่งเสริมสหกรณ์. กรุงเทพฯ: กรมส่งเสริมสหกรณ์.

กรมส่งเสริมสหกรณ์. (2554ก). ประเภทสหกรณ์. สืบค้นจาก https://cpd.go.th/content-page/item/1741-coop-type.html.

กรมส่งเสริมสหกรณ์. (2554ข). ความรู้ทั่วไปเกี่ยวกับสหกรณ์. สืบค้นจาก http://www.cpd.go.th/web_cpd/cpd_Allabout.html.

กรมส่งเสริมสหกรณ์. (2564). ประกาศรายชื่อสหกรณ์ขนาดใหญ่. สืบค้นจาก https://cpd.go.th/big-coop.html.

รุ่งนภา ทาธิวัน. (2563). การวิเคราะห์สภาพคล่องและความสามารถทำกำไรของบริษัทจดทะเบียนในตลาดหลักทรัพย์ เอ็ม เอ ไอ. (บริหารธุรกิจมหาบัณฑิต, มหาวิทยาลัยสุโขทัยธรรมาธิราช).

วารุณี ชายวิริยางกูร, สุกัญญา สีแดง, จิตราภรณ์ อุ่นแก้ว, ชัชชา บุ่งไธสง และ วิกรานต์ เผือกมงคล. (2563). ความสัมพันธ์ระหว่างสภาพคล่องและความสามารถการทำกําไรของธนาคารพาณิชย์ในประเทศไทย. วารสารบริหารธุรกิจ มหาวิทยาลัยแม่โจ้, 2(2), 46-59.

ศุภเจตน์ จันทร์สาส์น และ ธันยกร จันทร์สาส์น. (2565). ความสัมพันธ์ระหว่างสภาพคล่องและความสามารถในการทำกําไรของธุรกิจโรงแรมที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารปัญญาภิวัฒน์, 14(2), 57-73.

ศูนย์เทคโนโลยีสารสนเทศและการสื่อสาร กรมส่งเสริมสหกรณ์. (2566). รายงานจำนวนสหกรณ์. สืบค้นจาก https://itc.office.cpd.go.th/content_page/item/262-report-cooperatives.html.

สรฑัต ศรีวิชชพงษ์ และ ดารณี เอื้อชนะจิต. (2564). การบริหารสภาพคล่องที่ส่งผลต่อความเติบโตของกิจการของธุรกิจ ขนาดกลางและขนาดย่อมในประเทศไทย. วารสารมหาจุฬานาครทรรศน์, 8(11), 232–243.

สุภาวรรณ สุจารี และ จิรพงษ์ จันทร์งาม. (2565) อัตราส่วนสภาพคล่องและอัตราส่วนแสดงความสามารถในการทำกำไรที่มีอิทธิพลต่ออัตราส่วนมูลค่าตลาดของกลุ่มสินค้าอุตสาหกรรมของกิจการที่จดทะเบียนในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารสหวิทยาการมนุษยศาสตร์และสังคมศาสตร์, 5(4), 1284-1300.

อคิราภ์ กองจันดา. (2563). การวิเคราะห์เชิงเปรียบเทียบประสิทธิภาพของสหกรณ์ออมทรัพย์ในประเทศไทย. (บัญชีมหาบัณฑิต, มหาวิทยาลัยธรรมศาสตร์).

อินทร์ทิรา ภู่ระหงษ์. (2565) อิทธิพลของสภาพคล่องและความสามารถในการทำกำไรที่มีผลต่อการตัดสินใจในการลงทุนหลักทรัพย์ของบริษัทกลุ่มอุตสาหกรรมบริการในตลาดหลักทรัพย์แห่งประเทศไทย. วารสารรัฐประศาสนศาสตร์และการจัดการสังคม, 5(3), 384-406.

Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13(2), 187–221.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2025 Journal of Social Science Panyapat

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.