Exchange Rate Regimes and Inflation Transmission: Evidence from Hong Kong and Thailand

Keywords:

International Inflation Transmission, Cointegration, Vector Error Correction Model (VECM), Exchange Rate RegimeAbstract

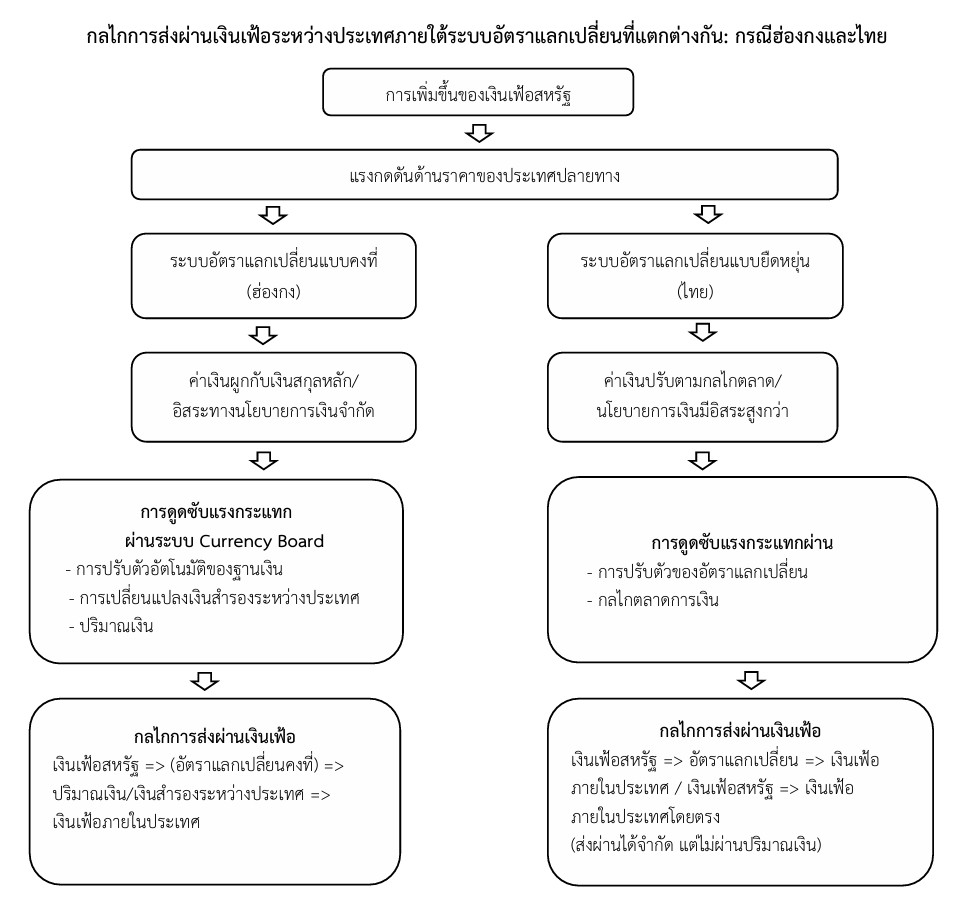

This study aims to (1) examine the long-run equilibrium relationship between U.S. inflation and Hong Kong inflation, (2) examine the long-run equilibrium relationship between U.S. inflation and Thai inflation, and (3) investigate the causal transmission of inflation from the United States to Hong Kong and Thailand. Monthly time-series data from January 2018 to December 2022 are employed, using the consumer price index, exchange rate, money supply, and international reserves as the key variables. The analytical methods consist of the Johansen Cointegration Test, the Vector Error Correction Model (VECM), and the Granger Causality Test. The empirical results show that (1) U.S. and Hong Kong inflation share a long-run equilibrium relationship, consistent with Hong Kong’s fixed exchange-rate regime, which limits monetary policy autonomy; (2) U.S. and Thai inflation also exhibit a long-run equilibrium relationship, indicating persistent price linkages despite Thailand’s managed-float regime; and (3) the transmission of U.S. inflation to Hong Kong operates through money supply and international reserves, whereas the transmission to Thailand occurs through domestic inflation and the exchange rate. Overall, the findings confirm that the exchange-rate regime plays a crucial role in shaping both the magnitude and channels of international inflation transmission, with fixed-rate economies being more exposed to global inflation shocks than economies with more flexible arrangements.

References

Cheung, Y.-W., & Yuen, J. (2002). Effects of U.S. inflation on Hong Kong and Singapore. Journal of Comparative Economics, 30(3), 603–619.

Choudhri, E. U., & Hakura, D. S. (2006). Exchange rate pass-through to domestic prices: Does the inflationary environment matter?. Journal of International Money and Finance, 25(4), 614–639.

Frankel, J. A., Parsley, D., & Wei, S.-J. (2012). Slow Pass-through Around the World: A New Import for Developing Countries?. Open Economies Review, 23(2), 213–251.

McCarthy, J. (2007). Pass-through of exchange rates and import prices to domestic inflation in some industrialized economies. Eastern Economic Journal, 33(4), 511-537.

Taylor, J. B. (2000). Low inflation, pass-through, and the pricing power of firms. European Economic Review, 44(7), 1389–1408.

Downloads

Published

How to Cite

Issue

Section

License

Copyright (c) 2026 Journal of Social Science Panyapat

This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License.